The market is not disappearing.

But the part of the market that operators and investors have historically relied on is.

For decades, hazardous waste has been understood as a downstream services industry, defined by collection, transportation, treatment, and disposal. Scale, asset ownership, and regulatory compliance were the primary drivers of advantage.

That framing is now incomplete.

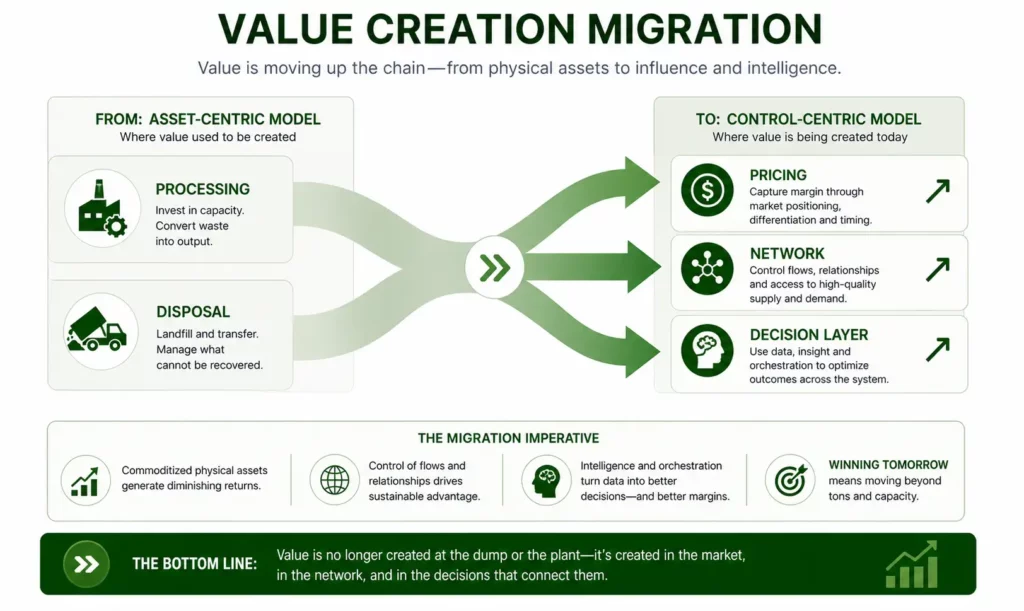

What is emerging instead is a structurally different system—one where value is increasingly created upstream, complexity is shifting downstream, and control is migrating to those who can manage the network—not just operate within it.

1. A Structural Shift: From Externalization to Internalization

At the core of this transition is a clear shift: Hazardous waste is increasingly being managed at the point of generation rather than through the external market.

Across chemicals and petroleum, waste is being redesigned into production systems through:

- Process re-engineering

- Recovery economics

- Regulatory pressure

The implication is fundamental: The most predictable and economically valuable waste streams are no longer entering the external market.

Understanding this shift requires more than operational visibility—it demands analytics that track how value is retained and how flows evolve.

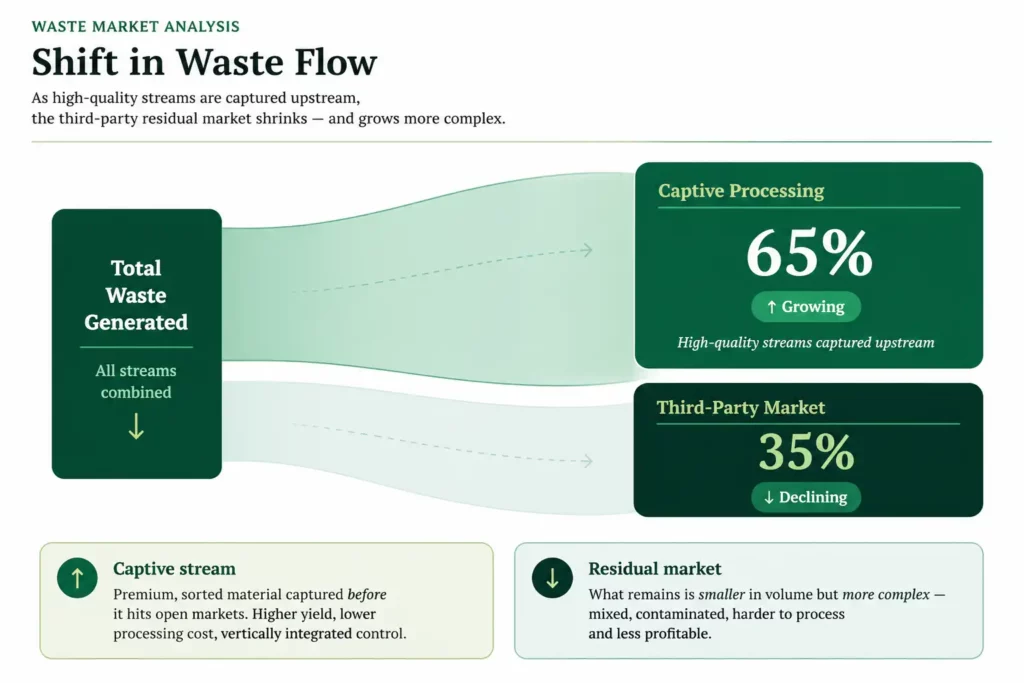

2. A Market That Appears Stable — but Is Not

At an aggregate level, hazardous waste volumes appear stable.

But underneath:

- Captive volumes are rising

- Third-party volumes are compressing

For operators, this distinction is critical.

Only the third-party market is monetizable—and that market is structurally shrinking.

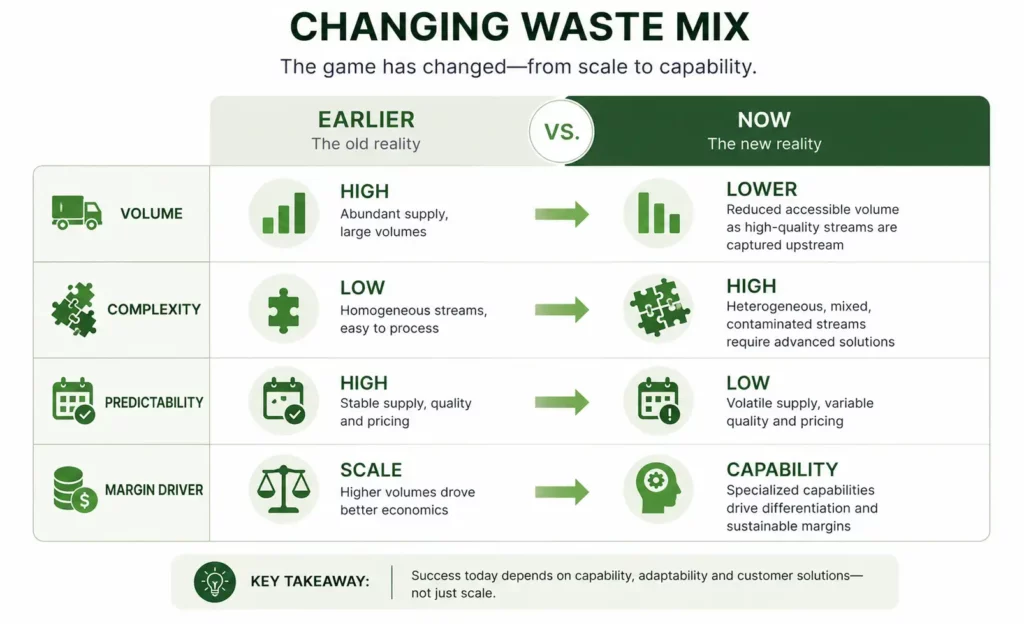

3. The Residual Market Is More Complex—and Less Forgiving

Historically:

- Large, homogeneous streams

- High recoverability

- Predictable generation

Increasingly:

- Smaller, mixed, contaminated streams

- Irregular flows

- Higher compliance burden

This marks a structural shift: From scale-driven processing to capability-driven complexity management

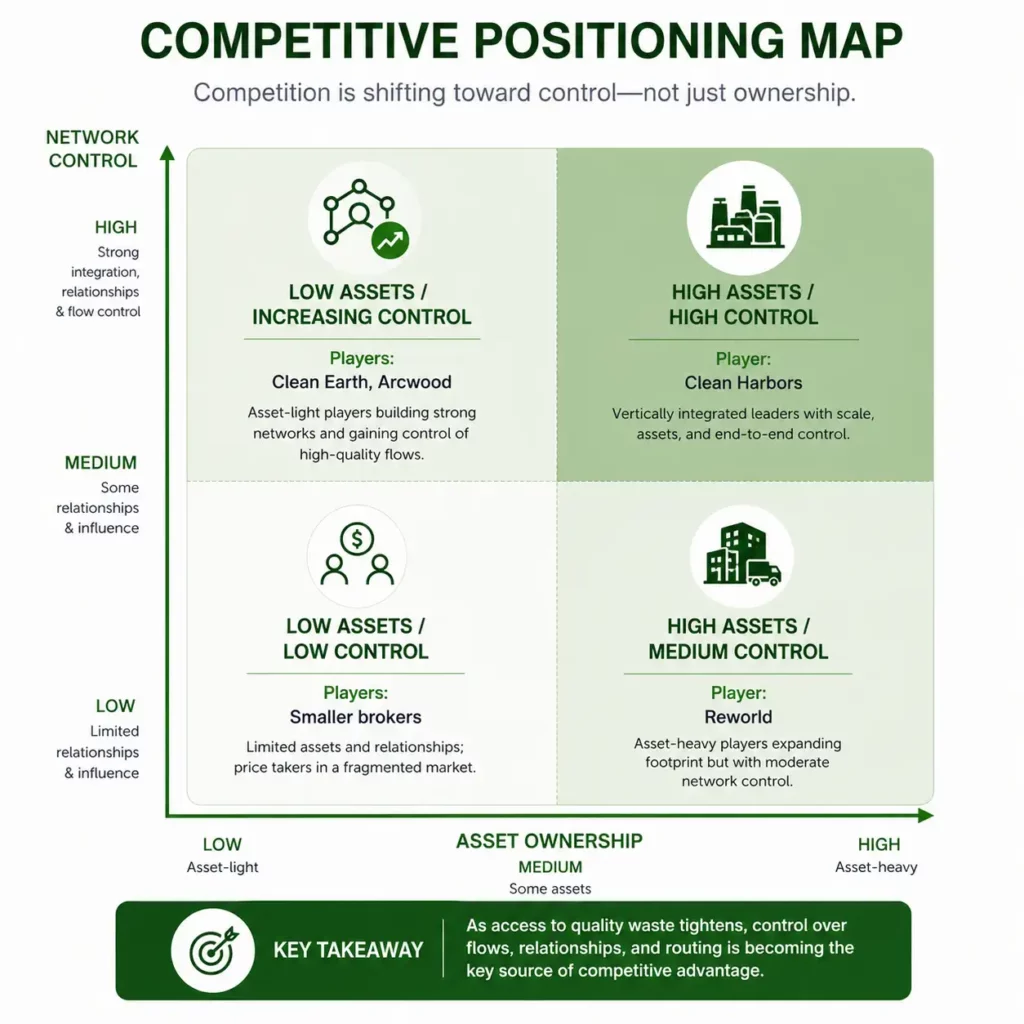

4. Where Leading Players Are Moving

Leading players are already repositioning—though not uniformly.

Integrated Players: Moving Upstream

Clean Harbors and Reworld are:

- Expanding direct generator relationships

- Leveraging disposal assets to control pricing

- Building integrated offerings

Reworld’s expansion beyond waste-to-energy signals a clear shift:

Own the waste stream earlier—not just process it later

Clean Harbors continues to:

- Anchor its model around incineration assets

- Expand field services and retail reach

- Use asset control to influence market dynamics

Broker Models: Being Reshaped

Players such as Clean Earth and Arcwood Environmental are navigating a different reality:

- Tightening access to disposal

- Increased competition from asset owners

- Pressure on traditional brokerage economics

In response, they are:

- Securing disposal access

- Driving pricing discipline

- Investing in internal systems and network coordination

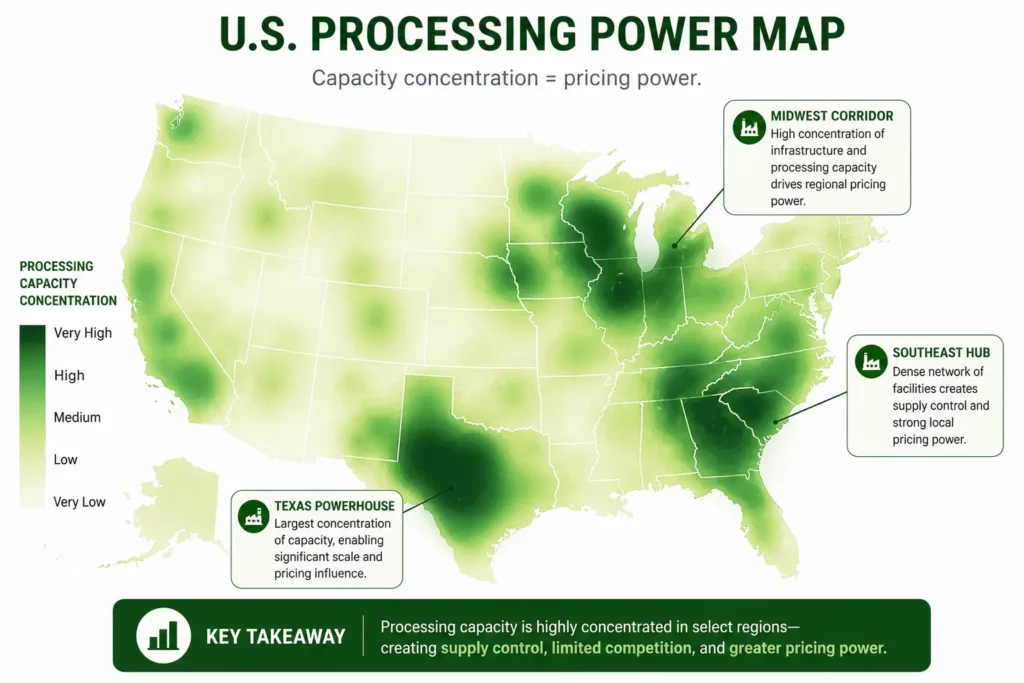

5. Geography Is Becoming Strategy

Processing capacity is increasingly concentrated in:

- Texas

- Midwest

- Southeast

These regions benefit from:

- Industrial density

- Favorable permitting

- Existing infrastructure

This creates:

- Bottlenecks

- Regional pricing power

- Dependency risks

These are no longer just operational realities—they are strategic signals surfaced through Waste Industry Data Intelligence.

6. The 3rd Party Model Is Being Rewritten

The combined effect of:

- Upstream capture

- Downstream complexity

- Capacity concentration

Is producing a market that is:

- Smaller in accessible volume

- Higher in complexity

- More dependent on network coordination

This is not cyclical.

It is a structural reallocation of value across the system.

Implications for Operators

1. Growth will not come from volume: Pricing, mix, and efficiency will drive outcomes

2. Disposal access becomes strategic: Control over capacity defines positioning

3. The network becomes the business: Operators are evolving into system orchestrators

4. Complexity becomes the margin driver: Handling difficult streams is the new advantage

In this environment, operators are shifting toward data-driven models where AI-Powered Analytics for Waste Management supports pricing optimization, routing efficiency, and capacity utilization.

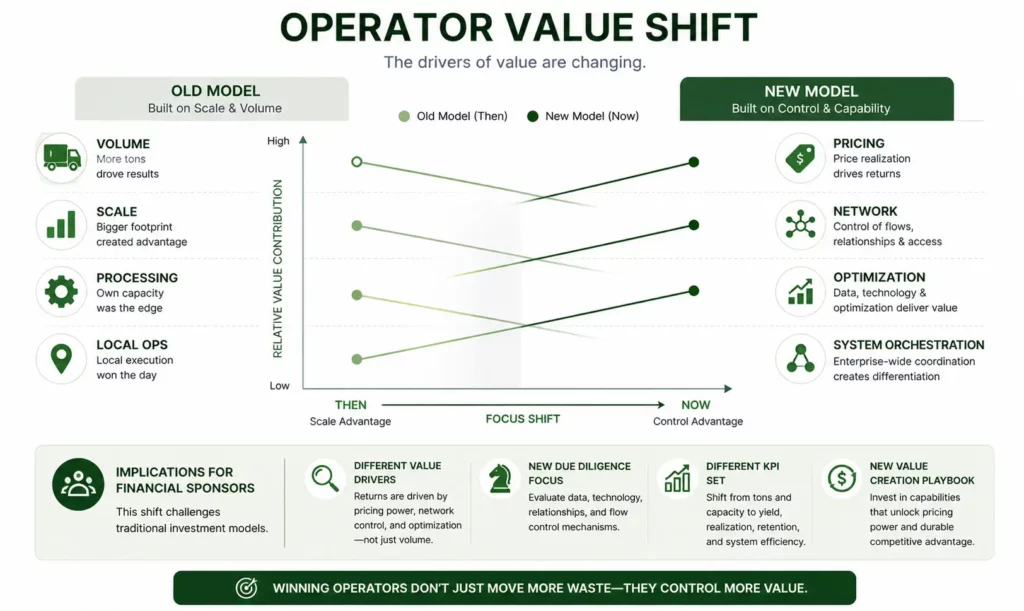

7. Implications for Financial Sponsors

This shift challenges traditional investment models.

1. Volume-led growth is fragile

Future growth is:

- Price-led

- Efficiency-driven

- System-dependent

2. Asset ownership is necessary—but insufficient

Winning requires:

- Access + integration

- Control overflows

3. Platform strategies must evolve

From:

- Geographic roll-ups

To:

- Network integration

- Decision capability

4. Value creation is moving upstream and system-wide

Returns will increasingly come from:

- Pricing optimization

- Capacity utilization

- Flow orchestration

A Shift from Industry to System

Hazardous waste is no longer a linear value chain. It is becoming a dynamic system of generators, facilities, routes, regulations, and pricing interactions.

In such a system:

- Constraints propagate

- Decisions are interdependent

- Value is created through coordination

Closing Perspective

Most operators—and many investors—are still structured for a world where:

- Volume was predictable

- Disposal was accessible

- Markets were local

That world is gone.

The next phase of the industry will not be defined by who can process the most waste.

It will be defined by: Who can understand—and optimize—the system behind the waste