Executive Summary

The waste management industry is entering a structural transition. For decades, competitive advantage has been defined by:

- Asset ownership

- Route density

- Scale within regional markets

These fundamentals remain important. But they are no longer sufficient. A new layer of competition is emerging—one that sits above assets and operations:

The ability to continuously make better decisions across the network, enabled by a Decision Intelligence Platform for Waste Management.

This shift is being driven by:

- Increasing complexity across waste streams

- Fragmented and evolving demand patterns

- Rising pressure on margins

- The availability of granular, external data

- The maturation of AI and decision systems

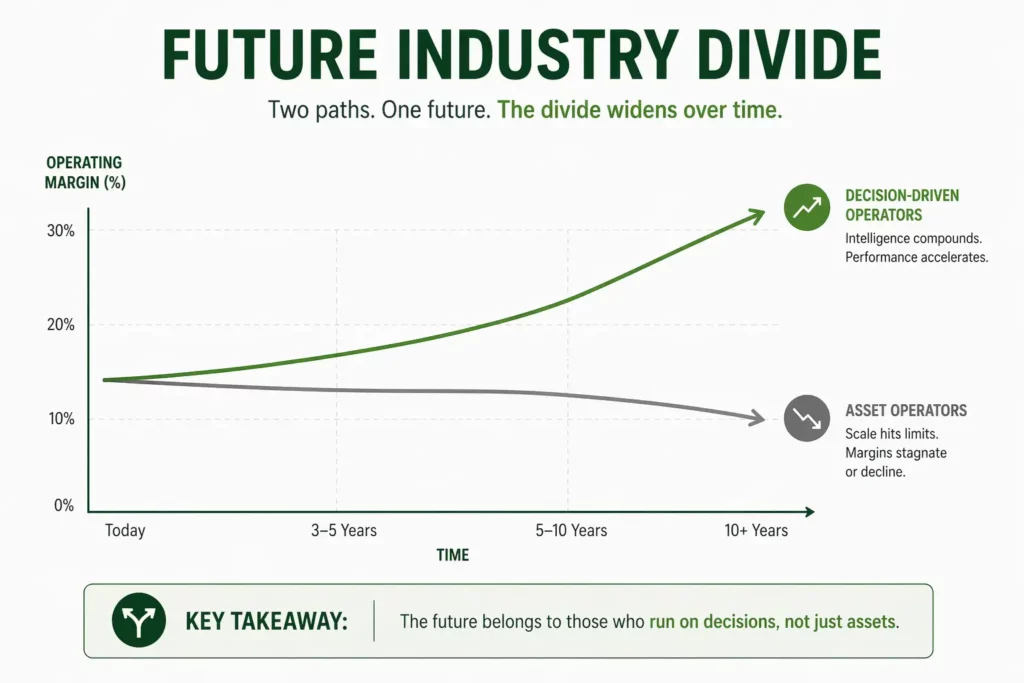

As a result, the industry is bifurcating into two distinct models:

- Asset Operators — focused on scale and execution

- Decision-Driven Operators — leveraging intelligence to optimize continuously

Over the next decade, it is the latter that will define industry leadership, powered by a Decision Intelligence Platform for Waste Management.

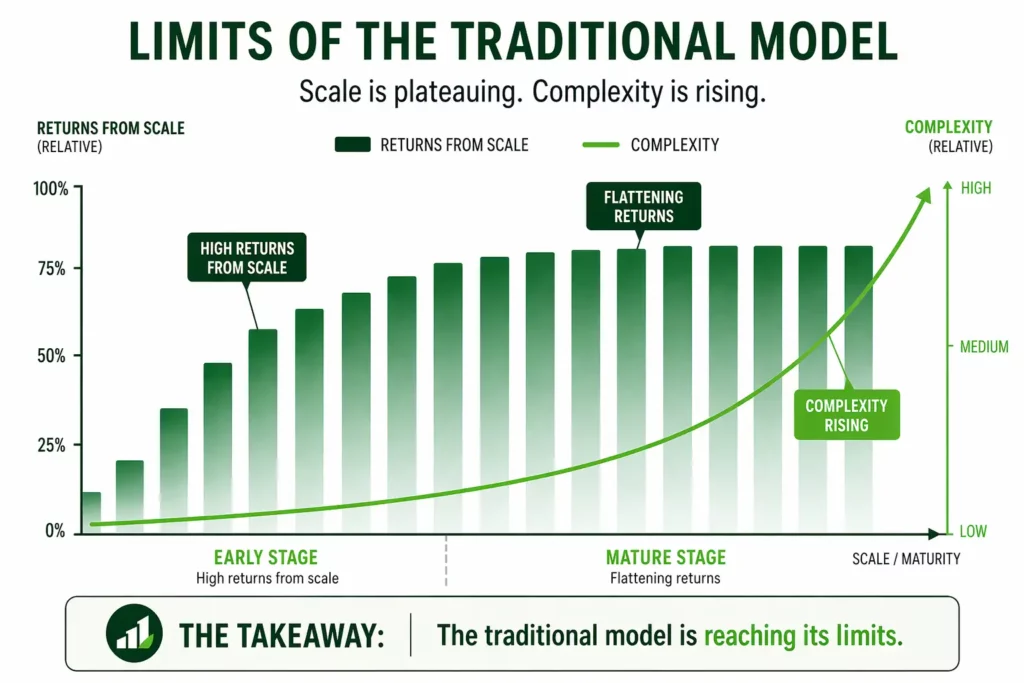

1. The traditional model is reaching its limits

The waste management industry has historically scaled through a well-understood playbook:

- Build or acquire assets (landfills, TSDFs, transfer stations)

- Increase route density

- Expand geographically through M&A

- Drive operational efficiencies

This model created significant value. However, structural constraints are now becoming visible, highlighting the need for a Decision Intelligence Platform for Waste Management.

1.1 Diminishing returns to scale

In many markets, incremental gains from density and scale are harder to achieve. Marginal routes are less profitable, and expansion often introduces complexity—challenges better addressed through a Decision Intelligence Platform for Waste Management.

1.2 Pricing opacity

Despite long-term contracts, pricing remains inconsistent across customers, geographies, and waste streams—limiting margin realization without a Decision Intelligence Platform for Waste Management.

1.3 Increasing operational complexity

Operators are now managing:

- Multiple waste categories (hazardous, liquid, organics, biosolids)

- Diverse customer segments

- Complex disposal and treatment pathways

These inefficiencies are often missed without a Waste Management Analytics Platform.

1.4 M&A fatigue

While consolidation continues, many deals fail to fully realize synergies due to limited integration at the network level. The result is a plateauing of traditional levers: Scale alone is no longer a sufficient driver of outperformance.

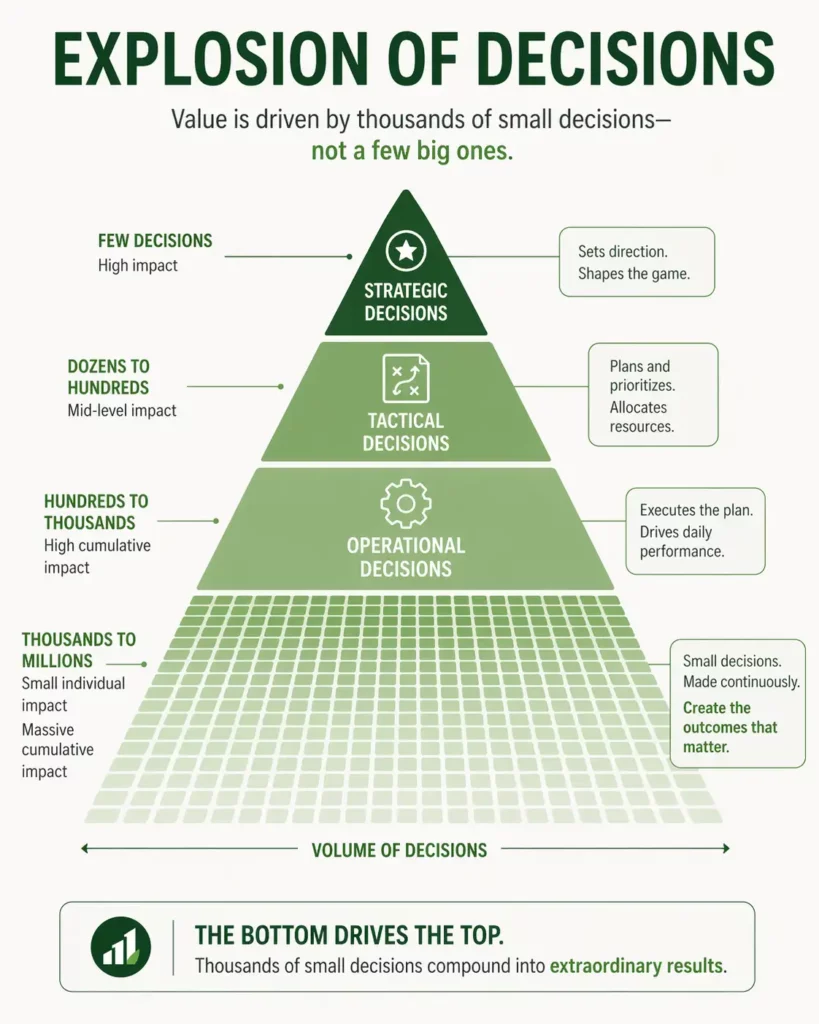

2. A new layer of competition is emerging

As traditional advantages plateau, a new differentiator is taking shape: Decision quality at scale.

Operators are increasingly required to make decisions that are:

- Frequent

- Interconnected

- Time-sensitive

- Economically significant

Examples include:

- Which accounts to target within a given region

- How to price services across similar customers

- How to optimize routes dynamically

- Where to deploy incremental capacity

- Which acquisitions improve network economics

Individually, these decisions are manageable.

Collectively, they define performance within a Decision Intelligence Platform for Waste Management.

Yet most organizations still manage them independently without a Decision Intelligence Platform for Waste Management, a gap increasingly addressed by AI-Powered Analytics for Waste Management.

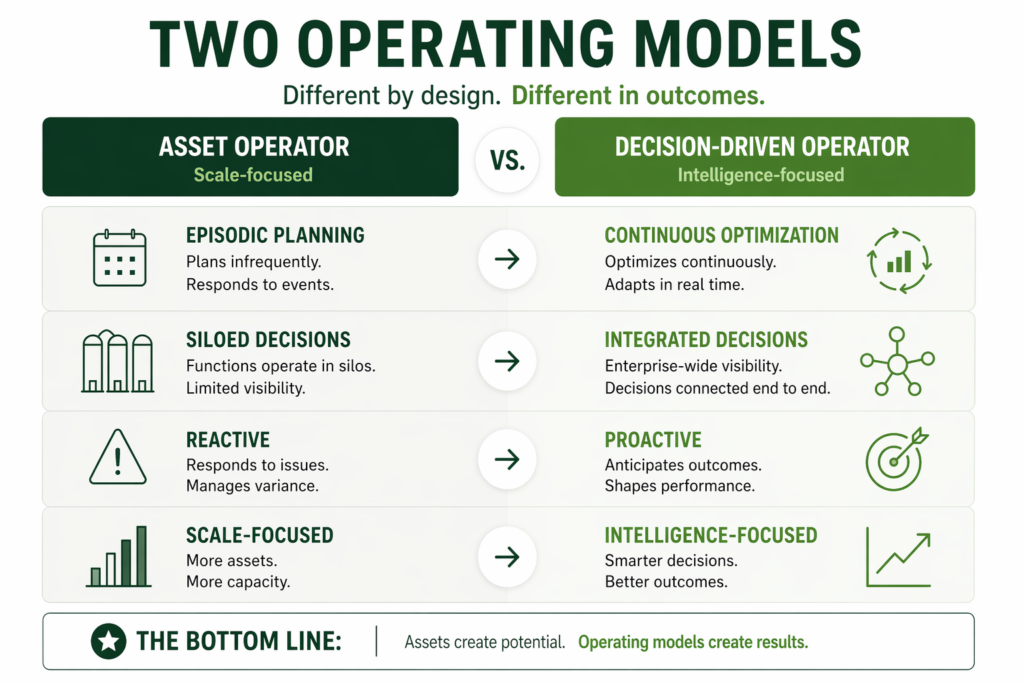

3. The rise of the Decision-Driven Operator

Leading companies are beginning to evolve beyond traditional operating models.

They are building capabilities to:

- Integrate internal and external data

- Continuously identify opportunities

- Prioritize actions by economic impact

- Embed insights into execution

This creates a new type of organization powered by a Decision Intelligence Platform for Waste Management: The Decision-Driven Operator

This model does not replace assets—it enhances their value through a Decision Intelligence Platform for Waste Management, while also enabling AI-Driven M&A in Environmental Services.

4. Five shifts that will define the next decade

The transition to decision-driven operations will manifest across five structural shifts:

4.1 From volume growth to yield optimization

Growth will increasingly come from:

- Better account targeting

- Cross-sell across existing customers

- Pricing precision

Rather than pure volume expansion.

4.2 From route efficiency to route economics

Operators will move beyond:

- Minimizing miles

To:

- Maximizing profitability per route

Incorporating:

- Transport costs

- Disposal economics

- Customer mix

4.3 From static pricing to dynamic pricing systems

Pricing will evolve from:

- Contract-driven

To:

- Continuously optimized

Based on:

- Market conditions

- Customer characteristics

- Competitive positioning

4.4 From episodic M&A to continuous network design

M&A will shift from:

- Opportunistic acquisitions

To:

- Network-driven strategy

Where each deal is evaluated based on:

- Impact on route density

- Asset utilization

- Cost structure

4.5 From internal data to integrated intelligence

Operators will expand beyond:

- Internal systems

To:

- External demand, supply, and market signals

Creating a more complete view of the ecosystem.

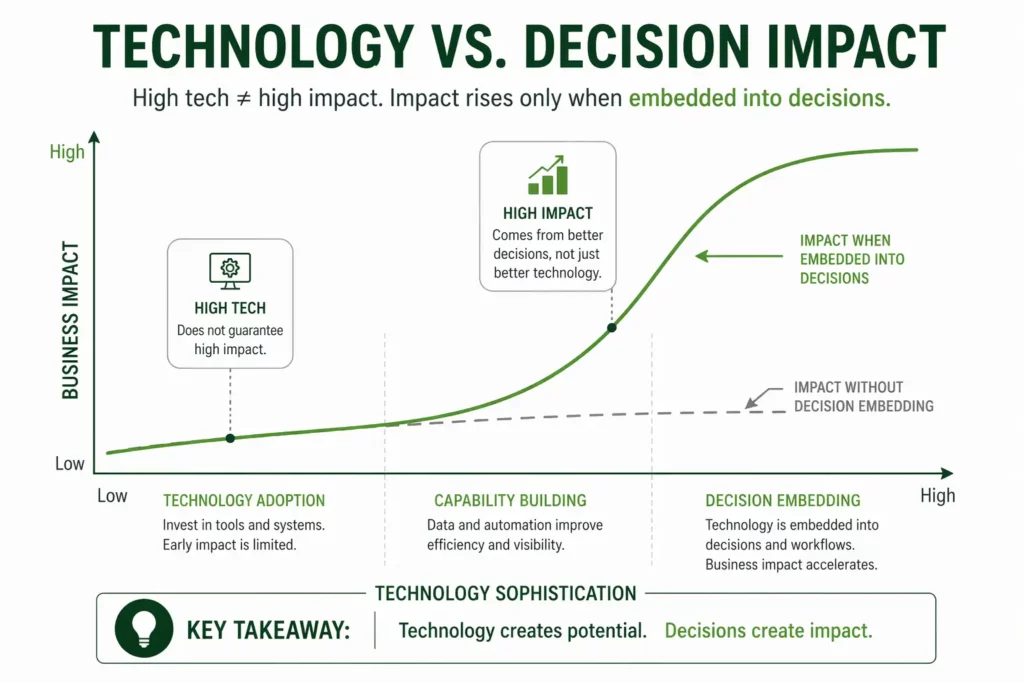

5. Technology as an enabler—not the answer

AI and data platforms are often positioned as the solution. In reality, they are enablers of a broader shift.

The critical change is not:

- Access to data

- Or the sophistication of models

It is: The ability to embed intelligence into everyday decisions without this, technology investments remain underutilized.

6. Implications for leadership teams

This shift has direct implications for CEOs, CFOs, and operating leaders:

CEOs: Must redefine competitive advantage beyond assets

CFOs: Gain new levers for EBITDA expansion through pricing, yield, and capital efficiency

COOs: Move from execution optimization to decision optimization

Strategy / M&A leaders

Transition to continuous network design

7. The winners of the next decade

The defining characteristic of leading operators will not be:

- Who owns the most assets

- Or who operates most efficiently

It will be: Who consistently makes the best decisions across the system?

These organizations will:

- Grow faster without proportional asset expansion

- Achieve higher margins

- Deploy capital more effectively

- Outperform in M&A

8. Conclusion

Waste management is transitioning from an asset-driven industry to a decision-driven one.

Assets will remain necessary but they will no longer be sufficient.

The next phase of value creation will be defined by:

- Continuous intelligence

- Integrated decision-making

- System-level optimization

The organizations that recognize and act on this shift early will define the next generation of industry leaders.

The future of waste management will not be determined by who owns the network.

It will be determined by who understands—and optimizes—it best.