Why annual investment themes and opportunistic sourcing are giving way to always-on origination systems

Executive Summary

However, while the process is structured, it is also episodic. Markets do not evolve annually—they shift continuously, driven by regulatory changes, infrastructure constraints, capital flows, and localized demand dynamics. As a result, investment themes, when treated as periodic outputs, quickly lose relevance.

This structural mismatch creates inefficiency at the front end of private equity.

A new model is emerging. Leading firms are combining continuous theme validation with systematic origination. This is not a marginal improvement—it is a structural shift. Firms that institutionalize this approach are not only increasing deal flow, but also improving timing, selectivity, and ultimately, investment returns.

The Structural Reality

Private equity firms often believe they compete on access, relationships, and execution speed.

In practice, most firms are operating with similar information, processed in similar ways, at similar points in time. The result is a convergence of behavior:

- The same sectors are targeted

- The same companies are approached

- The same processes are followed

- The same auctions are entered

This creates a false sense of differentiation. The implication is straightforward: firms that outperform will not be those that see more deals, but those that see the right deals earlier. This is not a function of effort—it is a function of infrastructure.

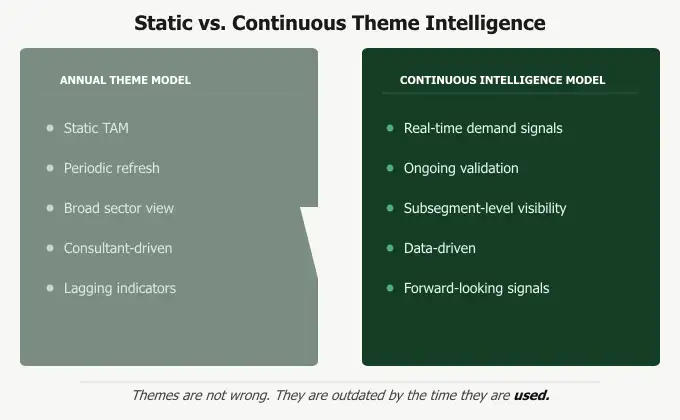

The Structural Limitations of Traditional Theme Development

The traditional approach to theme development is well established. Firms conduct periodic sector deep dives, often supported by consultants and internal research teams. These efforts result in detailed market maps, TAM estimates, and prioritized subsectors. While this process provides intellectual clarity, it rarely translates into a sustained sourcing advantage.

Four structural limitations explain why.

1. Static Market Assumptions

Total addressable markets are typically estimated at a single point in time and revisited infrequently, implicitly assuming stability. In reality, markets evolve continuously. Demand shifts across regions, infrastructure capacity tightens or expands, and margin dynamics change in response to competitive and regulatory pressures.

A static TAM provides a snapshot of where the market was—it does not indicate where opportunity is forming. As a result, firms relying on periodic analysis often identify opportunities only after they have become visible to the broader market.

2. Limited Capture of Forward-Looking Signals

Markets generate forward-looking signals continuously, including regulatory filings, facility permits, contract awards, capital expenditure announcements, and management transitions. Individually, these signals may appear incremental; collectively, they often indicate inflection points well before formal sale processes begin.

In most firms, these signals are neither captured nor structured systematically. Instead, sourcing remains dependent on intermediary visibility and relationship networks—delaying engagement and reducing information asymmetry.

3. Disconnection Between Themes and Target Universes

A persistent challenge in private equity is the lack of integration between thematic thinking and target identification. While a sector may be deemed attractive, firms often do not maintain a continuously updated universe of companies aligned with that thesis. Even when target lists are created, they are typically static and quickly outdated, and rarely prioritized based on strategic fit.

Without a dynamic link between themes and targets, investment theses remain conceptual rather than actionable.

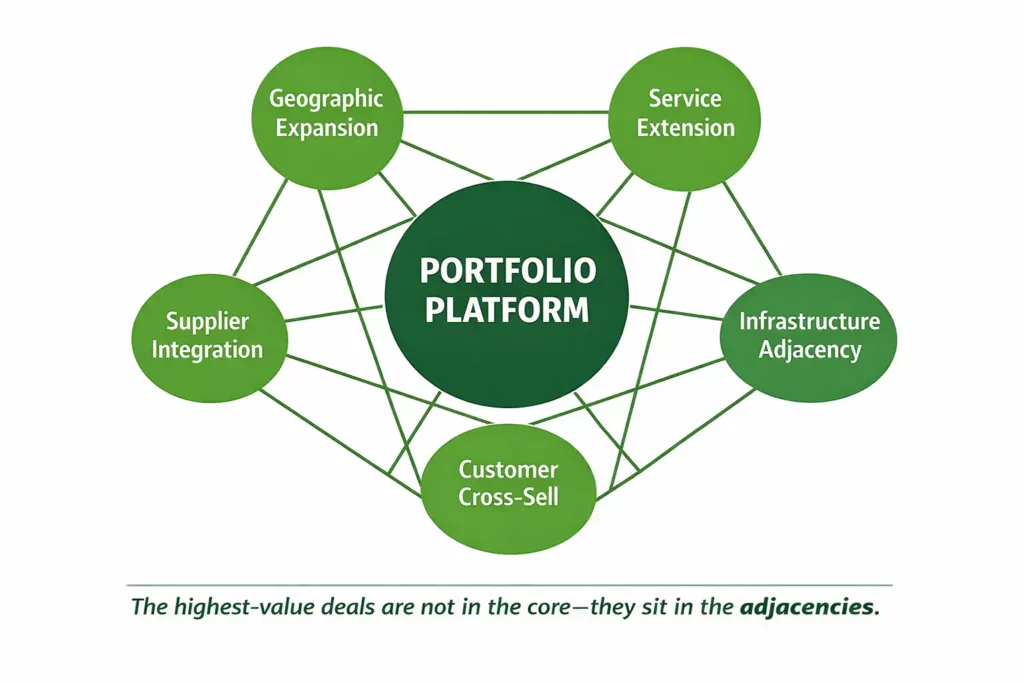

4. Underdeveloped Adjacency Modeling

Many of the most successful investments occur in adjacencies rather than core segments.

These adjacencies may include geographic expansion, service extensions, or infrastructure complementarity. Despite their importance, adjacency opportunities are often identified reactively.

Few firms operate systems that continuously map these relationships across markets and portfolio companies. As a result, adjacency discovery remains dependent on individual insight rather than institutional capability.

What We Are Seeing in the Market

Across fragmented, infrastructure-heavy sectors, several patterns are emerging consistently.

First, signals precede transactions by a meaningful margin. In multiple markets, regulatory filings, permits, and capacity expansions appear six to eighteen months before formal sale processes begin.

Second, the highest-value deals are increasingly adjacency-driven. Acquisitions that extend platforms into complementary geographies or services consistently outperform those confined to core segments.

Third, static target lists underperform. Firms that rely on periodic mapping of target universes are consistently late to engage with the most attractive opportunities.

These patterns suggest that sourcing advantage is no longer driven by access alone—it is driven by continuous visibility and early pattern recognition.

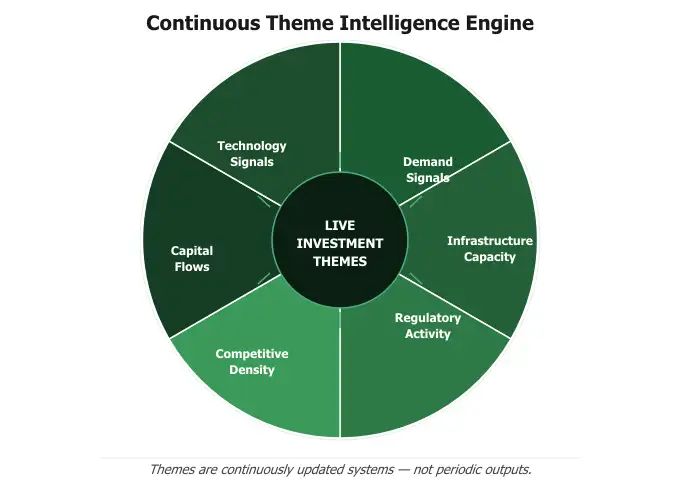

From Themes to Systems: Continuous Theme Intelligence

The structural shift required is straightforward in concept but significant in impact. Investment themes should not be treated as periodic outputs. They should be developed and maintained as continuous intelligence systems. A continuous theme intelligence model integrates multiple layers of information, including:

- Granular demand patterns across subsegments and regions

- Infrastructure capacity and utilization data

- Competitive density and market structure

- Regulatory and permitting activity

- Capital deployment trends

- Indicators of technological disruption

By integrating these inputs, firms can continuously validate—or invalidate—their investment theses.

This fundamentally changes decision-making. Conviction develops earlier. Subsegments are prioritized with greater precision. Sourcing becomes targeted rather than exploratory. Themes evolve from static narratives into origination engines

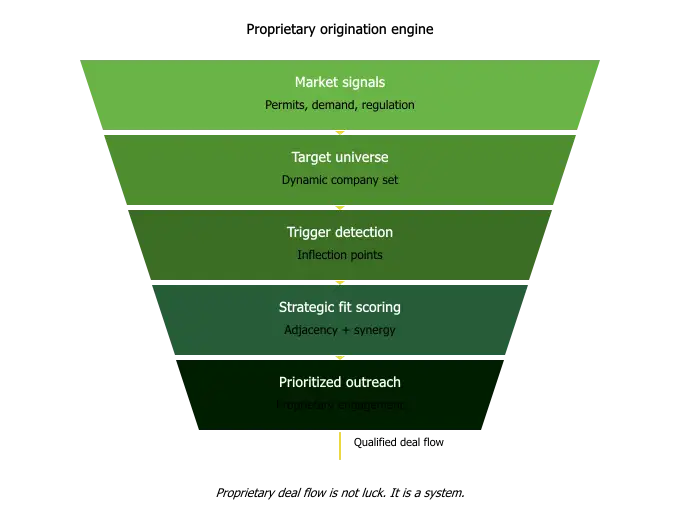

Systematizing Proprietary Origination

The aspiration to increase proprietary deal flow is nearly universal across private equity. However, in most firms, proprietary sourcing remains dependent on relationships, outreach, and timing.

Continuous Monitoring of the Target Universe

Rather than relying on static lists, firms maintain dynamic universes of companies segmented by revenue scale, geography, asset footprint, and service mix. These universes are continuously updated as new information becomes available. This ensures that the firm’s view of the market remains current and actionable.

Early Detection of Inflection Points

Structured monitoring of market signals enables firms to identify companies approaching strategic inflection points. These signals may include:

- Expansion permits or facility investments

- Regulatory pressures

- Changes in contract portfolios

- Shifts in management or ownership

Identifying these signals early enables firms to engage with targets before they enter competitive processes. This is the foundation of true proprietary access.

Systematic Prioritization Through Strategic Fit

Not all targets are equally relevant. Decision infrastructure enables firms to evaluate and rank companies based on their alignment with existing portfolio platforms. This includes:

- Adjacency to current services

- Geographic density

- Cross-sell potential

- Infrastructure complementarity

- Margin profile compatibility

The result is a continuously refreshed, prioritized pipeline of targets. Outreach becomes deliberate rather than opportunistic.

Pattern Recognition at Scale

Proprietary deal flow is often described as relationship driven. In reality, it is a function of pattern recognition. By monitoring structured signals across markets, firms can identify:

- Emerging regional clusters

- Fragmented subsegments

- Consolidation pressure

- Undervalued operators

When these patterns are identified early, firms gain a meaningful timing advantage. Proprietary sourcing becomes institutionalized rather than dependent on individual relationships.

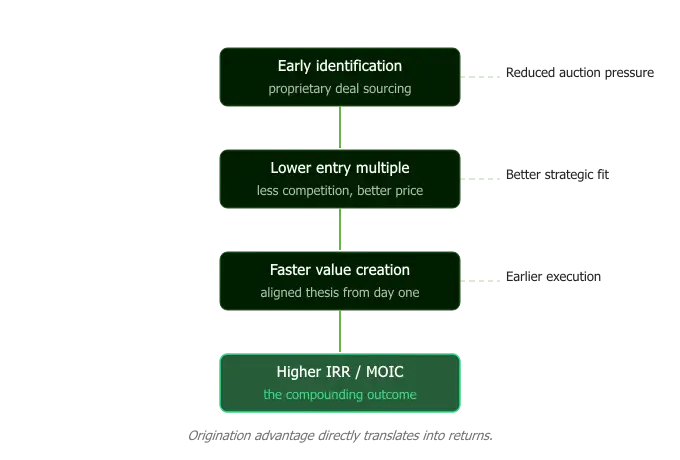

Translating Origination Advantage into Returns

Continuous origination is not simply a process improvement. It directly impacts investment performance through three mechanisms.

Entry Multiple Discipline

Earlier engagement reduces reliance on competitive auction processes. This leads to lower effective entry multiples and improved downside protection.

Revenue Synergy Realization

Targets identified through adjacency and strategic fit scoring exhibit stronger alignment with existing platforms. This increases the probability and speed of revenue synergies, including cross-sell and geographic expansion.

Time to Value Creation

When opportunities are identified and understood earlier, value creation planning begins pre-acquisition. This reduces the time required to activate pricing, operational, and commercial initiatives post-close.

In combination, these effects improve both IRR and MOIC, particularly in environments where multiple expansion is constrained. This is structural alpha—not driven by leverage, but by information and timing.

Strategic Implications for Private Equity Leaders

The front end of private equity is undergoing a structural redesign.

The relevant question is no longer, “How many opportunities did we evaluate?”

It is, “How early did we identify the right opportunities?”

Firms that continue to rely on episodic theme development and opportunistic sourcing will remain reactive. Those that invest in continuous, systematic origination will begin to anticipate market movements. Over time, this distinction compounds—better timing leads to better entry points, better entry points lead to stronger platforms, and stronger platforms enable more effective expansion.

The front end of private equity is no longer defined by access. It is defined by timing—and timing, increasingly, is a function of infrastructure.