Executive summary

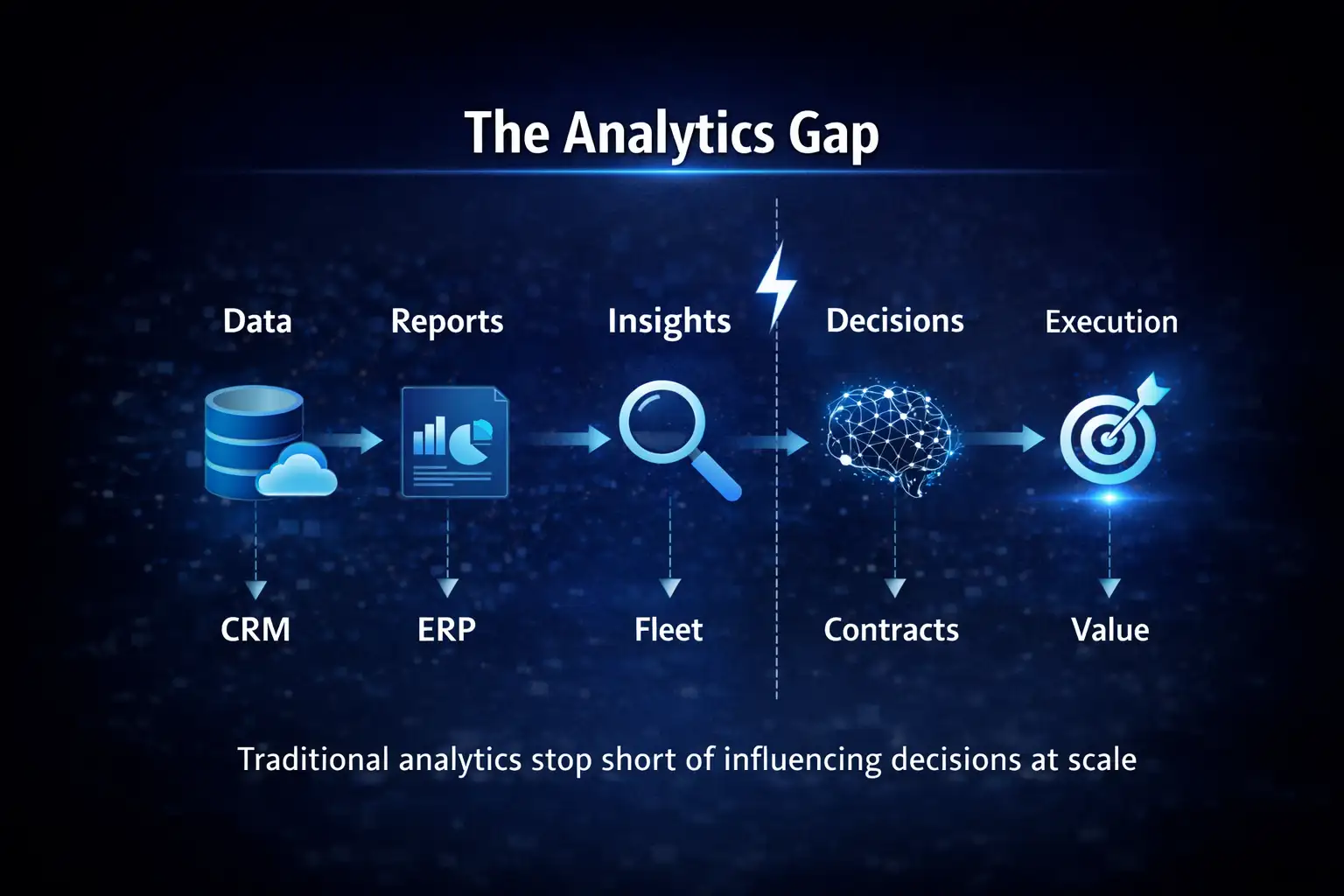

Waste management companies are not constrained by a lack of data. They are constrained by the inability to translate fragmented data into consistent, high-quality decisions at scale.

Across revenue growth, pricing, routing, asset deployment, and M&A, most operators continue to rely on a combination of static reporting, localized analysis, and institutional intuition. While this model has supported growth historically, it is increasingly misaligned with the structural complexity of the industry—characterized by multi-service offerings, geographically distributed networks, and tightening margin dynamics.

A new operating model is emerging: the Decision Intelligence Platform. It integrates internal and external data into an always-on system that continuously identifies, prioritizes, and quantifies decisions across the enterprise.

Early adopters are demonstrating meaningful impact, with 300–800 basis points of EBITDA improvement driven by simultaneous gains in revenue, pricing, asset utilization, and M&A effectiveness.

The implication is clear:

Over the next decade, competitive advantage in waste management will shift from asset ownership to decision quality and speed.

The structural problem: an industry built on fragmented decisions

Waste management is inherently a networked business. Revenue is generated at the account level, delivered through route networks, and monetized through disposal and processing assets. Each layer is interdependent.

Yet decision-making across these layers remains fragmented.

Sales teams pursue accounts based on local visibility. Pricing decisions are often anchored in historical contracts rather than current market conditions. Routing systems optimize for operational efficiency but rarely incorporate full economic context. Asset planning is based on capacity reports rather than forward-looking demand signals. M&A decisions are made episodically, with limited integration into network-level strategy.

This fragmentation creates a persistent disconnect:

Decisions are made at the point of activity, but value is realized at the level of the system.

The consequences are measurable:

- Underpenetrated accounts despite a significant installed base

- Systematic pricing inconsistencies across similar customers

- Route networks that are operationally efficient but economically suboptimal

- Capital deployed without full visibility into demand density

- M&A synergies that are modeled but not realized

These are not isolated inefficiencies. They are symptoms of a deeper issue:

The absence of a unified decision system

2. Why traditional analytics approaches are no longer sufficient

Most operators have attempted to address these challenges through incremental improvements:

- Additional reporting layers

- Point analytics solutions

- Periodic strategy exercises

While these efforts provide localized improvements, they do not fundamentally change how decisions are made.

Three structural limitations persist:

2.1 Episodic insight generation

Analysis is conducted periodically through quarterly reviews, annual planning, and ad hoc deep dives. As a result, decisions lag underlying changes in customer behavior, pricing dynamics, and route economics.

2.2 Lack of prioritization

Even when insights are generated, they are rarely ranked by economic impact. Organizations struggle to answer a basic question:

Which decisions should we act on first to maximize EBITDA?

2.3 Disconnection from execution

Insights are often not embedded into frontline workflows. Sales teams, pricing managers, and operations leaders continue to rely on existing processes, limiting real-world impact.

The result is an “analytics paradox”:

More data and more analysis—but limited improvement in outcomes.

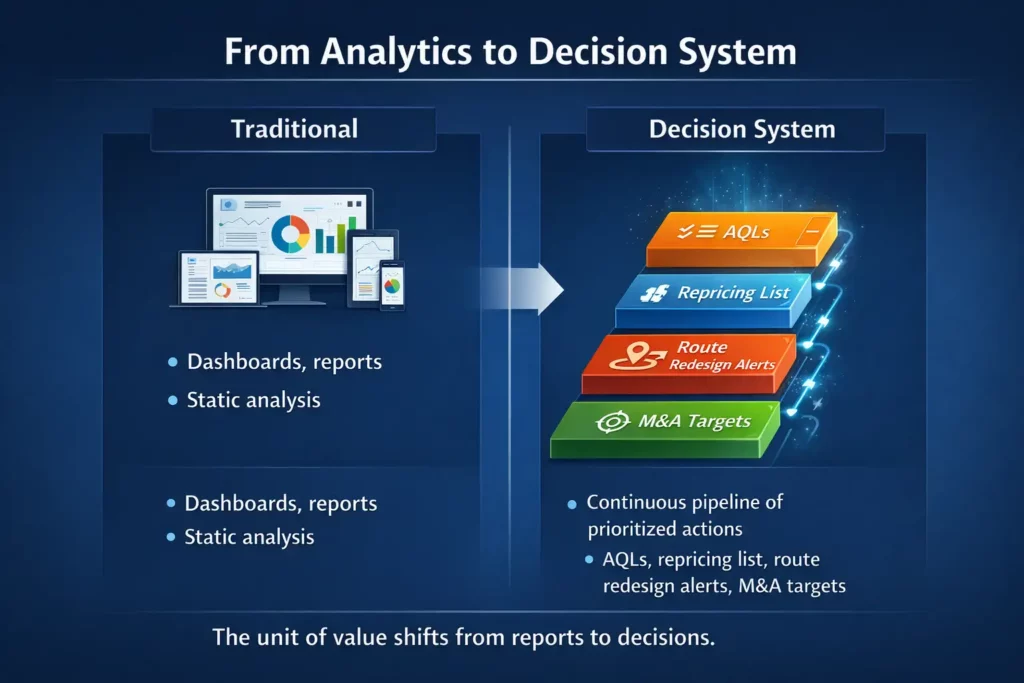

3. The shift: from analytics to a Decision Intelligence System

Leading operators are beginning to adopt a different paradigm—one that treats decision-making as a system rather than a set of isolated activities.

A Decision Intelligence System is defined by three characteristics:

- Always-on

Continuously ingests internal and external data to surface opportunities in real time

- Decision-centric

Organizes data around decisions (e.g., which accounts to target, which routes to redesign), not reports

- Actionable by design

Embeds prioritization, impact quantification, and workflow integration

This represents a shift from:

- “What happened?”

to - “What should we do next—and why?”

4. The Five Engines of a Decision Intelligence System

A comprehensive Decision Intelligence Platform in waste management operates across five interconnected domains. Each corresponds to a set of high-impact decisions that, when integrated, drive system-level value.

4.1 Revenue and yield intelligence: unlocking latent demand

Most operators underestimate the revenue potential embedded within their existing footprint. Accounts remain underpenetrated, cross-sell opportunities are not systematically identified, and acquisition efforts lack precision.

A decision-driven approach integrates:

- Generator-level demand signals

- Account-level service penetration

- Competitive and pricing context

This enables a structured progression from analytically qualified leads (AQLs) to conversion-ready opportunities.

Over time, revenue generation shifts from opportunistic selling to a repeatable, data-driven engine, powered by the Decision Intelligence System.

4.2 Asset and route intelligence: managing the economics of density

Route density is one of the most critical—and least visible—drivers of profitability in waste management.

Small shifts in customer distribution, service frequency, or routing patterns can significantly impact transport costs and asset utilization. However, these effects are rarely monitored in real time.

A Decision Intelligence Platform enables:

- Continuous detection of route density erosion

- Integration of transport, service, and disposal economics

- Dynamic route and fleet optimization

The focus shifts from operational efficiency to economic optimization at the route level.

4.3 Pricing and contract intelligence: capturing full economic value

Pricing in waste management is often constrained by legacy contracts and inconsistent benchmarking.

As a result, similar customers can be priced materially differently, and margin leakage persists across the portfolio.

A system-driven approach introduces:

- Corridor-level price benchmarking

- Detection of inconsistencies across accounts

- Prioritized repricing actions based on risk and impact

This transforms pricing from a reactive process into a continuous margin optimization lever, enabled by a Decision Intelligence System.

4.4 M&A origination and synergy: from episodic to continuous strategy

M&A remains a central growth lever in the industry. However, deal evaluation is often disconnected from network-level economics.

A Decision Intelligence Platform reframes M&A as an extension of operational strategy:

- Identifying targets based on route and asset adjacency

- Quantifying impact on network density and cost structure

- Tracking synergy realization post-close

This shifts M&A from opportunistic deal-making to a continuous, intelligence-driven capability.

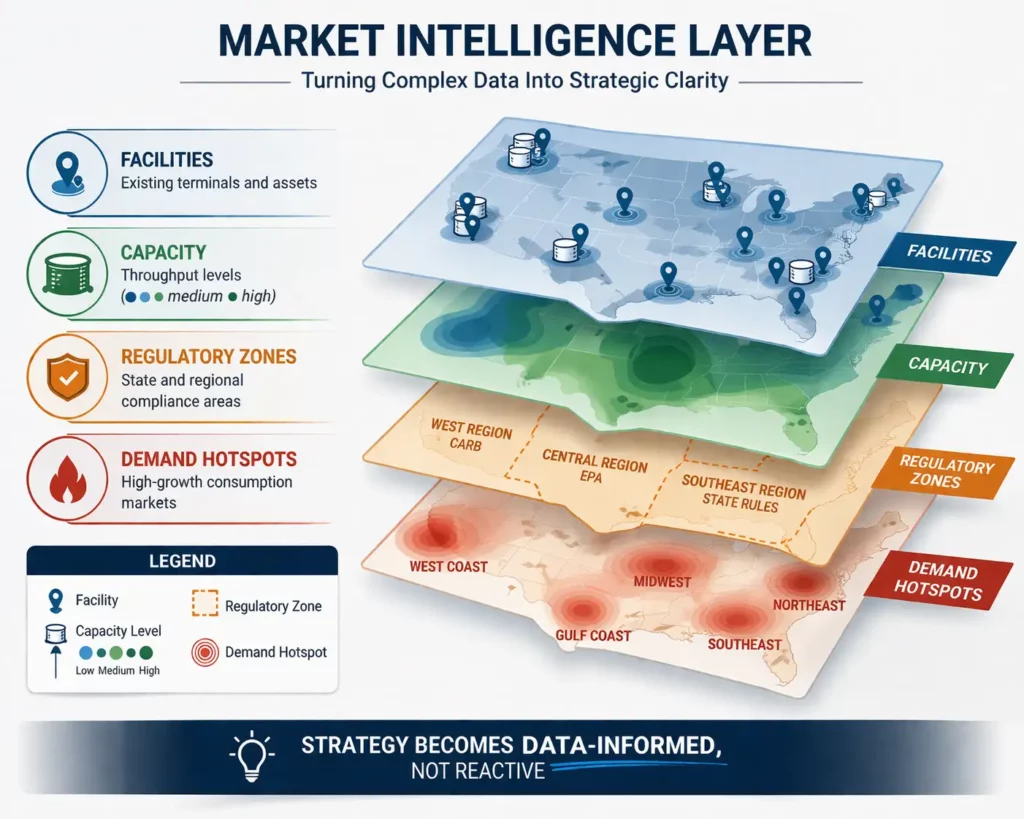

4.5 Market and competitive intelligence: anticipating structural shifts

External dynamics—capacity additions, regulatory changes, emerging waste streams—are increasingly shaping competitive advantage.

A decision system integrates these signals into strategic planning, enabling operators to:

- Identify emerging high-value waste streams

- Anticipate capacity constraints

- Position ahead of competitors

5. Economic impact: a multi-lever EBITDA transformation

The value of a Decision Intelligence Platform is not derived from a single use case, but from the compounding impact across multiple decision domains.

A typical value bridge includes:

- Revenue uplift (5–15%)

Driven by cross-sell, improved conversion, and targeted acquisition - Pricing improvement (5–10%)

Through systematic repricing and benchmark alignment - Cost optimization (3–8%)

Via route and asset efficiency gains - M&A uplift (variable)

Through improved deal selection and integration

In aggregate, this translates to:

300–800 basis points of EBITDA expansion

6. Implementation: a pragmatic path to scale

Despite its strategic implications, implementation does not require a large-scale transformation upfront.

Leading operators follow a focused approach:

Step 1: Targeted pilot (4–6 weeks)

- Single geography

- 1–2 decision domains

- Clear financial metrics

Step 2: Regional scaling

- Expand across geographies

- Integrate additional datasets

Step 3: Enterprise deployment

- Extend across all decision domains

- Embed into workflows

This approach ensures early value realization while building toward a system-wide capability.

7. The emerging divide: asset operators vs decision-driven operators

As the industry evolves, a clear distinction is emerging between two types of operators:

Asset-centric operators

- Focus on scale and footprint

- Rely on traditional decision processes

- Experience margin pressure over time

Decision-driven operators

- Leverage integrated intelligence

- Continuously optimize across the system

- Achieve superior growth and profitability

The implication is profound:

Competitive advantage will increasingly be defined not by asset ownership, but by the ability to make better decisions—consistently and at scale.

8. Conclusion

Waste management is entering a new phase of evolution.

The next frontier is not operational efficiency alone, but decision excellence—the ability to continuously identify, prioritize, and execute the highest-value actions across the enterprise.

The organizations that build Decision Intelligence Platform will not only improve performance; they will redefine how the industry operates.