For decades, the U.S. biosolids industry operated as a relatively legible system. Wastewater treatment plants generated sludge. That sludge was dewatered, hauled, and moved through one of four well-established pathways: land application, landfill, incineration, or composting. The competitive logic was straightforward — manage volume efficiently, maintain regulatory compliance, and secure disposal contracts. Scale mattered. Geography mattered in a relatively simple way. The business functioned largely as a linear pipeline with a limited number of endpoints.

That model no longer reflects operational reality.

The endpoints still exist, but the system around them has changed enough to fundamentally alter how the market functions.

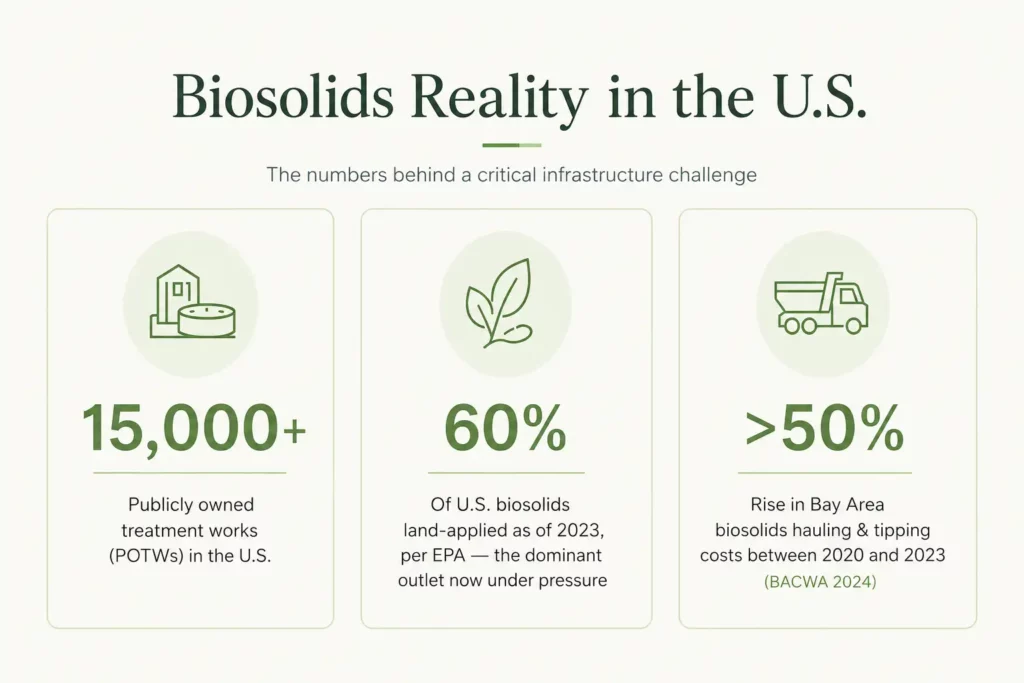

More than 15,000 publicly owned treatment works (POTWs) operate across the United States. Roughly 60% of U.S. biosolids were still land-applied as of 2023, according to the EPA, making it the dominant outlet despite increasing pressure. At the same time, Bay Area biosolids hauling and tipping costs rose by more than 50% between 2020 and 2023, according to BACWA’s 2024 Biosolids Trends Report.

BACWA’s survey of 32 Bay Area wastewater agencies revealed more than rising unit costs. It showed a broader operational shift underway. Agencies are hauling biosolids farther, relying on additional offsite treatment, and moving away from disposal pathways that no longer function the way they once did. Nearly all Bay Area agencies had stopped using landfill alternative daily cover (ADC) by 2015, partly in response to California’s SB 1383 organic waste diversion mandates. Yet 57% of biosolids still ended up in landfills in 2023.

The implication is important: constraining disposal pathways without creating scalable alternatives does not eliminate landfill dependency. It simply increases the cost of maintaining it.

That dynamic — tightening disposal options, rising costs, and no obvious replacement — is not unique to California. It increasingly defines the U.S. biosolids market. In some regions, operators and investors are responding by building new infrastructure and recovery capacity. In others, operators are still running the legacy disposal model while absorbing escalating costs.

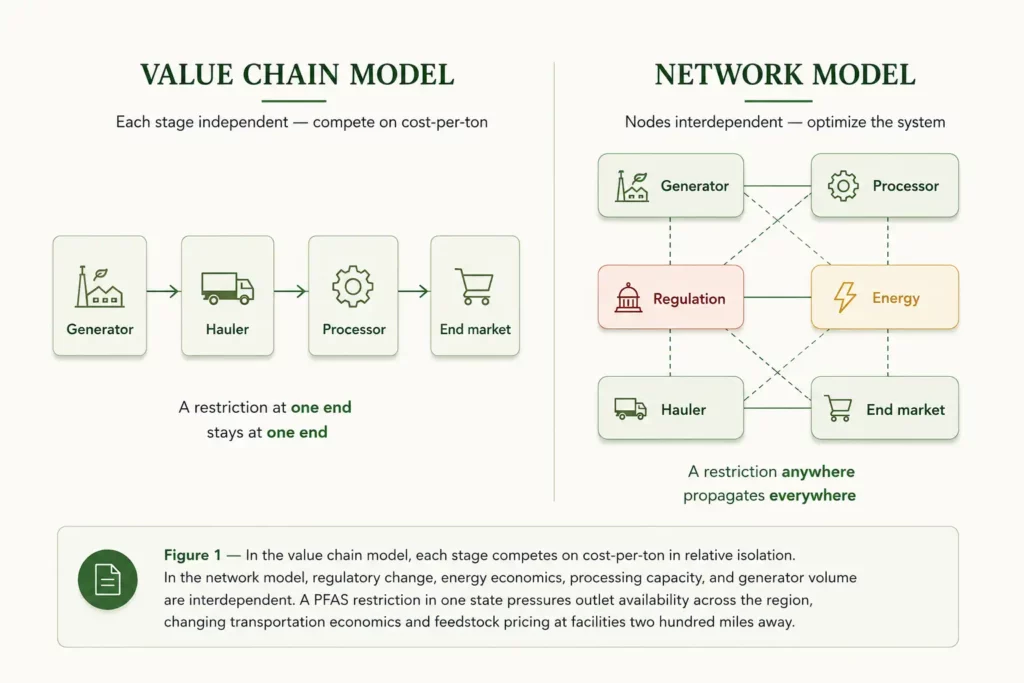

From Pipeline to Network

The traditional biosolids model treated the industry as a linear value chain. Generators produced volume. Haulers transported it. Processors treated it. End markets absorbed it. Each stage operated relatively independently.

Under that model, the economics of a hauling company were not materially affected by downstream processing constraints several counties away. Likewise, a processing facility’s economics were not closely tied to changing regulatory conditions affecting generators in neighboring states. Operators competed largely on cost-per-ton efficiency within a specific stage of the chain.

The emerging network model functions differently.

A regulatory change that restricts land application in one state does not remain localized. It redirects volume flows, pressures hauling capacity across regions, alters disposal pricing, and changes feedstock availability for digestion and recovery facilities upstream. Technology decisions are increasingly interconnected with market conditions as well. Higher energy values and stronger RNG economics can shift a facility from a disposal-oriented model toward a resource recovery model centered on biogas, electricity generation, or renewable natural gas production.

The system is now interconnected, and regulatory, commercial, and operational decisions propagate through it.

This distinction matters because competitive advantage changes fundamentally between the two models.

In a linear value chain, the lowest-cost operator at a specific step often wins. In a networked system, operational efficiency alone becomes insufficient. Durable advantage comes from the ability to optimize the system as a whole — understanding where outlet capacity exists, which regulatory environments are tightening, which generator relationships are exposed to future constraints, and which routing and recovery configurations maximize margin across the broader network.

Why Traditional Disposal Pathways Are Becoming Less Viable

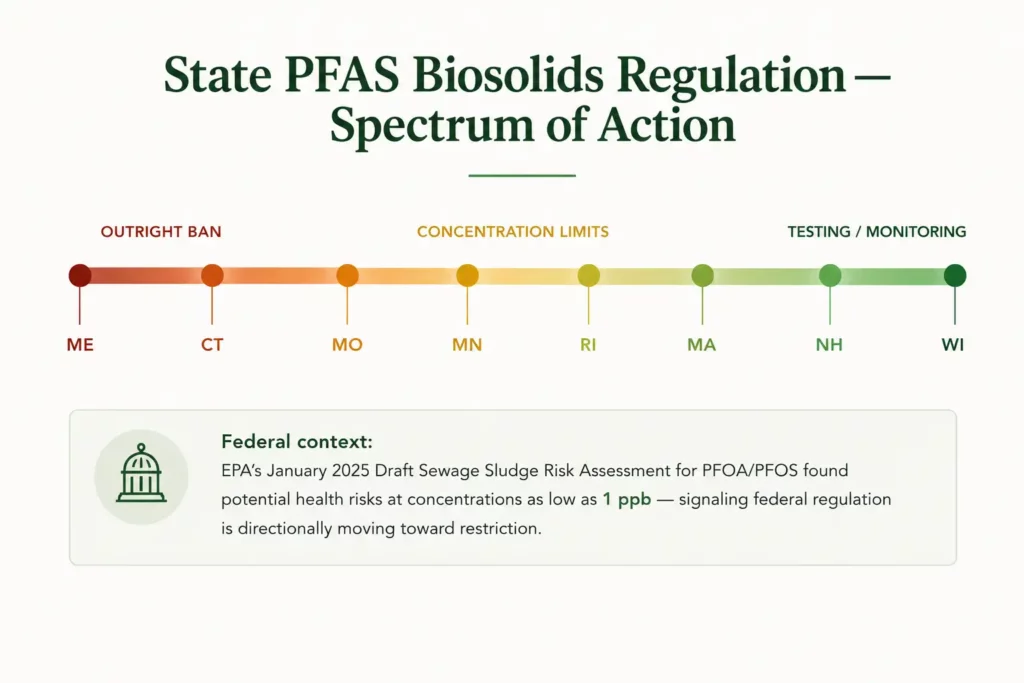

PFAS regulation is now reshaping the economics of traditional biosolids disposal.

As recently as 2023, roughly 60% of U.S. biosolids were land-applied. For decades, land application represented the dominant and lowest-cost disposal route. That assumption is becoming increasingly unstable.

Maine has implemented a complete ban on land application of biosolids. Minnesota now requires PFAS testing for biosolids intended for land application, including mandatory response actions above concentration thresholds. Maryland established PFAS concentration limits for PFOS and PFOA in sewage sludge used for land application. Connecticut banned biosolids sales containing PFAS for land application, while Rhode Island mandates quarterly PFAS sampling and state reporting requirements.

The EPA’s January 2025 Draft Sewage Sludge Risk Assessment for PFOA and PFOS identified potential health risks at concentrations as low as 1 part per billion under common land application scenarios. Although federal standards remain unfinished, the broader direction is increasingly clear: policy is moving toward tighter restrictions, not looser ones.

States are already advancing ahead of federal action, creating a fragmented regulatory environment that operators must navigate without long-term certainty regarding future compliance obligations.

Landfill pathways face pressure for different reasons.

California’s SB 1383 mandated a 75% reduction in landfill organic waste disposal by 2025, limiting both landfill ADC usage and conventional disposal practices. BACWA’s 2024 survey illustrates the operational consequences. Agencies that stopped using ADC did not discover a seamless alternative. Instead, they encountered higher transportation costs, more constrained outlet access, and rising disposal expenses.

This is the structural force accelerating interest in energy recovery and advanced processing infrastructure. Not because those technologies are ideologically preferred, but because legacy disposal pathways are simultaneously becoming more constrained and more expensive.

Recovery Capacity Is Becoming Strategic Infrastructure

The movement toward energy recovery is not solely regulatory. The economics themselves have shifted.

Between 2020 and 2024, U.S. RNG capacity grew by approximately 170%, with operational facilities increasing from 338 to 914 by mid-2025. Biogas infrastructure investment exceeded $2 billion in 2025, driven partly by corporations sourcing RNG from wastewater treatment systems to meet sustainability targets.

Programs such as the federal Renewable Fuel Standard and California’s Low Carbon Fuel Standard have transformed biogas-to-RNG conversion into a meaningful revenue stream rather than an operational byproduct.

Research from the American Society of Civil Engineers has demonstrated the economic impact of co-digestion. Combining biosolids with food waste or FOG produces substantially greater energy output at lower overall energy costs compared to biosolids digestion alone. While co-substrate systems require additional capital investment, the increase in energy yield materially changes facility economics.

DC Water’s Blue Plains facility remains one of the most visible examples. By integrating thermal hydrolysis pretreatment into its digestion system, the facility transformed what had historically been a disposal cost center into a materially stronger energy and biosolids recovery platform.

Generate Upcycle provides another large-scale example. In 2024, the company recycled approximately 1.1 million tons of organic waste, produced 490,000 gigajoules of RNG, and invested $30 million to expand its Cayuga Digester in Auburn, New York. Once completed, the expansion is projected to support 1.5 million gigajoules of annual RNG capacity.

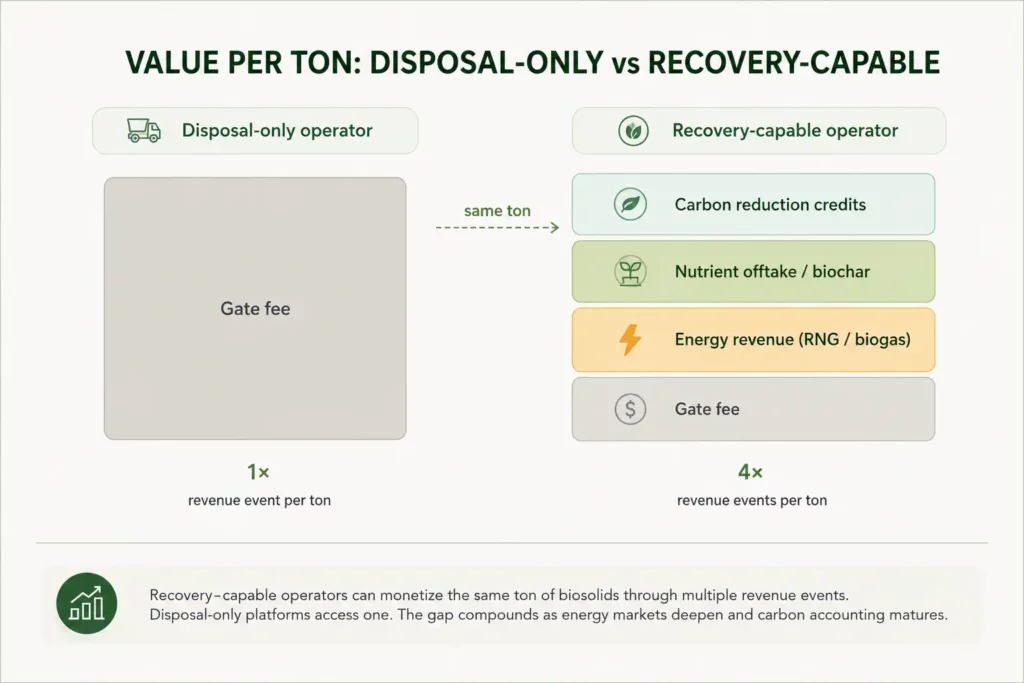

This is not a marginal enhancement to a disposal business. It is a fundamentally different business model built on the same material stream.

The strategic implication is straightforward: two operators with identical throughput, comparable geographic footprints, and similar generator relationships can still have dramatically different financial profiles depending on whether they possess recovery infrastructure.

Recovery-capable platforms monetize the same ton multiple times. Disposal-only platforms monetize it once — through outlets that are becoming progressively more expensive and constrained.

Why Distributed Processing Matters

Infrastructure industries naturally tend toward centralization. Large facilities benefit from economies of scale, and centralized anaerobic digestion systems have historically appeared more efficient than smaller regional assets.

That assumption is increasingly being tested by current operating realities.

Centralized systems are vulnerable to regulatory concentration risk. If a major processing facility depends heavily on land application access within a state that tightens PFAS restrictions, the system has limited flexibility. Volume continues arriving, but outlet availability disappears.

A distributed processing network offers greater resilience.

Regional processing nodes connected through intelligent routing systems allow operators to shift material across multiple regulatory environments, processing technologies, and outlet types. Material can be redirected toward alternative recovery systems, digestion infrastructure, or regions where regulatory conditions remain more favorable.

Co-digestion economics strengthen the case further.

Anaerobic co-digestion performs best when multiple organic feedstocks — food waste, FOG, agricultural residuals, and industrial organics — can be blended with biosolids. A single centralized facility is rarely positioned near all of those feedstock streams simultaneously. Distributed infrastructure, designed around actual waste generation geography, can often achieve more stable feedstock optimization and methane yields.

The utilization gap reinforces the opportunity. According to the American Biogas Council, only about 24% of facilities large enough to support anaerobic digestion currently capture and utilize biogas.

This is not primarily a technology limitation. Anaerobic digestion is already a mature industrial process. The constraint is infrastructure design, siting, logistics, and network coordination.

Facilities such as Anaergia’s Rialto Bioenergy Facility in California demonstrate how distributed feedstock aggregation models can operate at regional scale by integrating food waste and biosolids from multiple surrounding geographies into centralized RNG conversion infrastructure.

Volume Intelligence as Competitive Infrastructure

The transition from a linear pipeline to a distributed network fundamentally changes what operators need to know to make effective decisions.

Under the legacy model, understanding volume largely meant understanding how much tonnage contracted generators produced and where it was being disposed. That was sufficient because the system was relatively stable and routing options were limited.

In a networked environment, that information alone is insufficient.

Operators increasingly need near real-time visibility into regional generator volumes, regulatory exposure by geography, available processing capacity, pricing conditions, transportation economics, and downstream outlet availability. More importantly, they need to continuously model how those variables interact under changing market conditions.

The critical operational question becomes: where will the next constraint emerge, and what is the optimal infrastructure position when it does?

The Water Environment Federation’s 2026 Residuals, Biosolids and Innovations in Treatment Technology Conference reflects this shift directly. Its agenda centers heavily on PFAS monitoring integration, nutrient recovery economics, and infrastructure optimization at a system-wide level.

These are no longer isolated facility problems. They are network coordination problems.

This is where intelligence infrastructure becomes strategically important.

Operators capable of continuously tracking generator risk exposure, modeling routing scenarios against changing disposal availability, and identifying infrastructure or acquisition targets based on network positioning rather than simple throughput metrics gain a structural advantage in capital allocation, pricing, and operational flexibility.

That advantage compounds over time.

What Operators and Investors Are Actually Building Toward

The transition from a pipeline model to a network model does not eliminate the importance of traditional competencies. Generator relationships, hauling efficiency, and regulatory compliance remain foundational.

They are simply no longer sufficient.

Growth increasingly depends on infrastructure positioning rather than disposal volume alone. Operators are being pushed toward building or acquiring recovery capacity, securing flexible outlet access across multiple regulatory jurisdictions, developing co-digestion ecosystems, and implementing intelligence systems capable of optimizing routing and recovery economics across regional networks.

The individual facility increasingly functions as a node within a larger system, and its value is increasingly tied to the quality of the network it participates in.

For investors, the evaluation framework must evolve accordingly.

A platform processing 500,000 tons annually with limited outlet diversity, no energy recovery capability, and no intelligence layer may ultimately be structurally weaker than a smaller platform operating distributed recovery assets, co-digestion infrastructure, RNG offtake agreements, and dynamic routing capabilities.

Scale still matters. It simply no longer determines strategic value on its own.

Infrastructure positioning — including outlet control, recovery yield, regulatory resilience, and network density — increasingly does.

The biosolids market, valued at approximately $5.4 billion in 2025, is projected to reach roughly $7.6 billion by 2032, driven substantially by the expansion of resource recovery infrastructure and recovery-oriented processing models.

That growth will not distribute evenly across the market.

It will concentrate among the operators building recovery capacity, distributed processing systems, and the volume intelligence capabilities required to optimize increasingly interconnected infrastructure networks.

The critical question for operators and investors is no longer whether the transition is happening.

It is whether they are building for the network or still operating for the pipeline.