The next frontier in liquid waste is not operational, it is systemic

The liquid waste management industry spans UCO, grease traps, grit traps, jetting, plumbing, oily water, and industrial wastewater. Historically, operators have managed it as a route-based services business. They optimized trucks, routes, depots, and customer contracts at the local level.

That model is now reaching its limits.

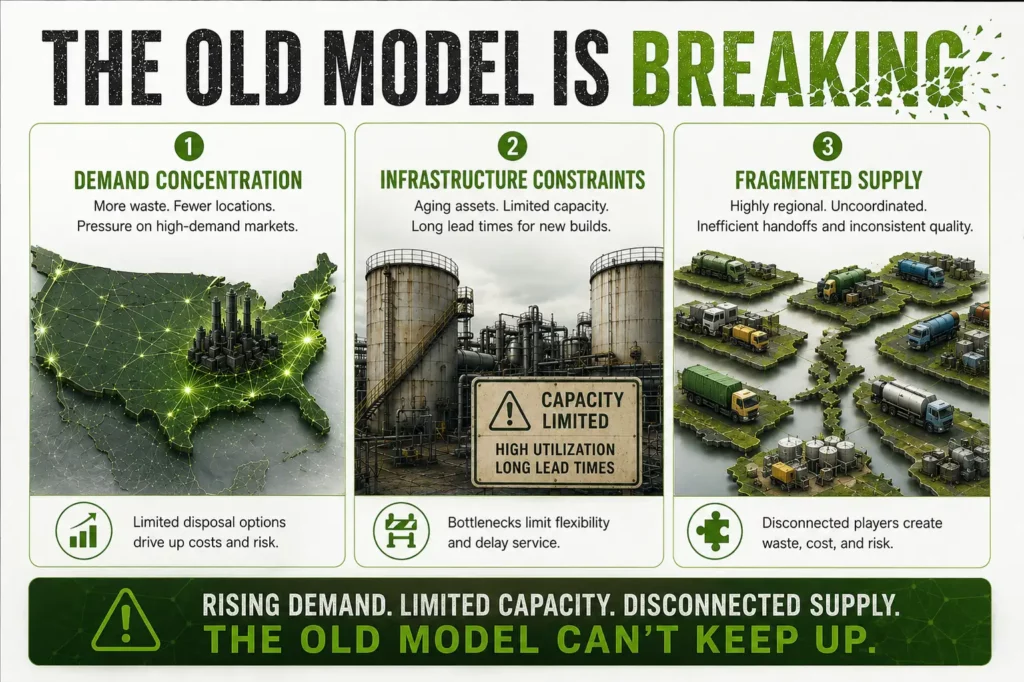

Across the US, the sector is undergoing a structural shift driven by three forces:

- Demand concentration: Waste generation is highly clustered in urban corridors and industrial zones

- Infrastructure constraints: Disposal outlets (Type V, POTWs, recycling) are finite and unevenly distributed

- Fragmented supply: Thousands of sub-scale operators with localized footprints

The implication is clear: Value is no longer created at the route level—it is created at the network level.

Yet most operators still manage the business through disconnected levers: sales, pricing, operations, and M&A. Without a unified decision system, growth becomes inefficient, margins leak, and capital is misallocated.

The result: suboptimal growth, margin leakage and misallocated capital.

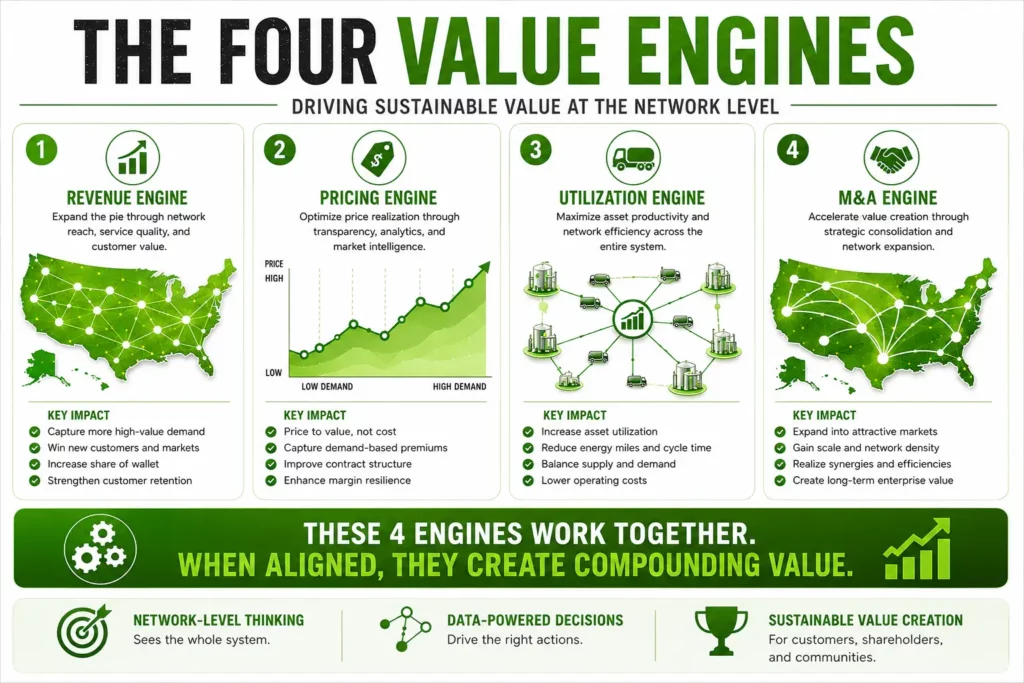

The four strategic engines of value creation

Leading operators are now reorganizing their businesses around four integrated value engines:

- Revenue acceleration

- Pricing optimization

- Asset utilization

- M&A strategy

Together, these engines shift the business from local route management to network-driven value creation.

1. Revenue Acceleration: From reactive service to demand capture

Core issue: Growth is constrained not by market size but by visibility into demand and conversion ability.

- Operators lack granular visibility into generator-level demand (who, where, how much, what type)

- Sales remains relationship-driven rather than data-driven targeting

- Cross-sell across services (e.g., grease + jetting + plumbing) is under penetrated

What differentiates leaders:

- Mapping demand at the site-level across industries and geographies

- Building structured funnels: AQL → MQL → SQL

- Driving route-adjacent acquisition, not random account wins

Impact: 10–15% revenue uplift without adding assets—purely from better demand capture.

2. Pricing: From static rates to market-aligned yield optimization

Core issue: Pricing remains blunt—often cost-plus or legacy-based—while the market is highly dynamic.

- Significant price dispersion across similar customers

- Weak linkage between pricing and route economics

- Limited understanding of elasticity and competitive positioning

What differentiates leaders:

- Pricing linked to proximity, service complexity, and disposal economics

- Dynamic benchmarking vs local competitors and alternatives

- Integration of pricing with routing and asset utilizatio

Impact: 5–10% pricing uplift with minimal churn, and improved margin consistency

3. Asset Utilization: From fleet efficiency to network efficiency

Core issue: Operators optimize trucks—but not the system.

- Suboptimal route density → high cost per stop

- Deadhead miles due to fragmented coverage

- Underutilized disposal optionality

What differentiates leaders:

- Designing contiguous service corridors, not isolated routes

- Integrating routing with demand density and disposal locations

- Treating assets (fleet + outlets) as part of a network graph

Impact: 20–30% improvement in route efficiency and asset productivity

4. M&A: From opportunistic deals to network design

This is where the industry is most misunderstood—and where the largest value pools exist.

Deep Dive: M&A as a Network Strategy, Not a Deal Strategy

The problem with traditional M&A in liquid waste

Most M&A strategies in the sector follow a familiar pattern:

- Broker-led processes

- Opportunistic acquisitions

- Financial screening (revenue, EBITDA, growth)

- Limited integration planning

This approach consistently misses value because it ignores the core economic driver of the business: network effects.

What the data actually shows

From our analysis, for a major operator:

- Only ~33% of addressable demand is covered, leaving 67% as whitespace opportunity

- Demand is highly concentrated in a few corridors, not evenly distributed

- Supply is deeply fragmented, with hundreds of local operators and service providers

This creates a structural opportunity: Selective acquisitions can disproportionately improve coverage, density, and pricing power.

In fact, targeted M&A can increase coverage from 33% → 51% with a limited set of acquisitions

Reframing M&A: From “Which company?” to “What network outcome?”

The right starting point is not the target—it is the network gap.

Step 1: Build full market visibility

- Map all generators (e.g., restaurants, industrials, energy facilities)

- Overlay waste volumes, types, and frequency

- Identify high-density demand corridors

(Example: 370K+ generators mapped in Texas with volume and location granularity )

Step 2: Overlay supply and infrastructure

- Operator footprints (depots, routes)

- Disposal infrastructure (Type V, POTWs, recycling)

- Permit and regulatory constraints

This creates a unified view of demand × supply × infrastructure

Step 3: Apply network filters (the real drivers of value)

From the LES framework (page 13): ~90% of M&A value is driven by network economics

Key drivers:

- Route density impact (25%) → lowers cost per stop

- Demand alignment (20%) → ensures real volume capture

- Outlet access (20%) → drives pricing power

- Proximity to network (15%) → accelerates integration

This fundamentally changes how targets are evaluated.

The three types of high-value acquisitions

Every target should be classified based on its role in the network:

1. Density Plays (route economics)

- Fill gaps in high-density corridors

- Increase stops per route

- Reduce deadhead miles

Outcome: Immediate cost and margin improvement

2. Outlet Plays (margin control)

- Add or secure disposal capacity

- Reduce reliance on third-party outlets

- Improve pricing flexibility

Outcome: Structural margin expansion

3. Capability Plays (service expansion)

- Add services (e.g., oily water, industrial cleaning)

- Expand into adjacent verticals

- Enable cross-sell

Outcome: Revenue growth + wallet share expansion

From long list to actionable targets

A systematic approach narrows the universe:

- Start with full market (all operators)

- Apply network filters → identify relevant geographies

- Apply strategic filters → ownership, deal readiness

- Rank and segment into:

- Tier 1 (10–15 targets): immediate acquisitions

- Tier 2 (20–30): strategic pipeline

- Tier 3: monitor

Why this approach wins

Traditional M&A answers: “Is this a good company?”

Network-driven M&A answers: “Does this asset improve our system?”

That distinction is decisive.

Because in liquid waste:

- Value is created through adjacency, not scale alone

- Integration is operational, not financial

- Synergies are spatial (routes, outlets), not just cost-based

The integration advantage (where most value is lost)

Even when deals are well-selected, value is often lost post-close.

A network-driven approach solves this upfront:

- Integration is pre-modeled through route adjacency and demand overlap

- Synergies are quantified in terms of density, pricing, and utilization

- Execution is aligned to operating teams, not just corporate development

From episodic M&A to a continuous system

The end-state is not a better pipeline—it is a different operating model.

As outlined in the LES framework:

- M&A becomes a continuous, always-on system

- Integrated across:

- Origination

- Prioritization

- Diligence

- Integration

This transforms M&A from a periodic activity into a core growth engine.

What this means for operators and sponsors

For operators

- Stop viewing M&A as expansion

- Start viewing it as network design

For private equity

- Move from deal sourcing to systematic origination

- Underwrite based on network impact, not just EBITDA

For management teams

- Align commercial, operations, and M&A under a single decision layer

- Measure success through:

- Coverage

- Density

- Outlet control

- Yield per route

What comes next

This is the first in a series.

If M&A is the structural lever, then:

- Revenue Acceleration is the demand engine

- Pricing is the yield engine

- Asset Utilization is the efficiency engine

Each will be explored in depth in subsequent articles.

Bottom line

The liquid waste industry is not a services business—it is a network optimization problem.

Those who continue to operate locally will remain subscale.

Those who build decision systems across demand, pricing, assets, and M&A will define the next generation of leaders.